Charter Communications

Company Overview

Charter Communications is the second largest US cable operator providing pay television, internet, and voice services to residential and business customers. Through its Spectrum brand, Charter operates in 41 states with a dense footprint in segments of the Northeast, upper Midwest, and Southeast regions of the country. In 2016, after acquiring Time Warner Cable (TWC) & Bright House Networks for roughly $71 billion, Charter quadrupled its footprint and currently has over 32 million active subscribers (subscribed to at least 1 service) and over 55 million passings equating to 58% penetration.

Cable Headwinds

With the rise of streaming services, the advancement of fiber optics and fixed wireless access (FWA), and the growth of the mobile market, Charter Communications’ business model has been under attack. The expansion of Netflix, Amazon Prime Video, and other streaming services has led to a decline in cable pay TV subscriptions. Since 2013, US pay TV subscriptions have declined by roughly 35 million to 65 million subscribers and by 2027 it is expected that there will be fewer than 48 million cable pay TV subscribers. “Cord cutting” has become a real headwind for Charter with video subscribers declining over 15% to 14.5 million since 2016. The company has responded by cutting expenses and trying to offset the revenue decline by offering more bundled services to its subscriber base. Ultimately, the profit margins on pay TV subscriptions have dwindled as higher content fees, customer service expenses, and network fixed costs are being spread across fewer subscribers.

Charter Communications is also seeing ongoing threats from the expansion of fiber optics and FWA in key markets and rural areas. Fiber optics is a superior product to traditional cable. It produces faster upload and download speeds, lower latency, higher security, requires less maintenance, and is more reliable, but there is a steep cost to lay the fiber. Today, fiber optics covers approximately 40% of Charter’s footprint primarily in highly dense urban and suburban areas. Because of the ongoing threat, Charter Communications is currently in the process of upgrading its entire network from DOCSIS 3.1 to DOCSIS 4.0 at a cost of $5.5 billion or $100/passing. Charter operates an HFC (Hybrid Fiber Coax) network that uses fiber to connect the headend station (distribution center) to fiber nodes. The “final mile” from the node to the home is connected via coaxial cable. In addition to the DOCSIS upgrade, Charter is also splitting its spectrum to provide higher upload speeds. After the work is completed, Charter expects its network to have a base of 2GB upload and 1GB download speeds. This pales when compared to the 10x10 symmetrical upload and download speeds that fiber operators are advertising.

The latest threat to Charter Communications is from FWA (fixed wireless access). FWA uses radio frequencies to deliver 5G broadband internet speeds to the home. This technology is predominantly found in rural areas of the country where cable & fiber passings are often limited or unavailable and DSL remains the only option. The two main providers of FWA in the US are T-Mobile and Verizon who, together, have amassed over 4 million subscribers in a short period of time. FWA subscriptions have been growing steadily over the past few years, whereas Charter’s broadband subscription growth has been slowing down.

MVNO (Mobile Virtual Network Operator)

Charter Communications became a MVNO when it launched its mobile service in late 2018. Providing mobile service to its subscriber base has been a growth opportunity for the company as its mobile subscribers have quickly grown to over 5 million users. A MVNO is a provider of wireless services that does not own or maintain the wireless network infrastructure. In short, Charter Communications entered into an agreement with Verizon to purchase bulk access to its wireless network at wholesale prices. Charter then offers those services to its 32 million customers either as a stand-alone plan or bundled with its other services (Broadband, Video, or Voice). Since Charter does not incur any maintenance or service fees, its cost of providing the wireless service is lower than the wireless carriers, and since it is not restricted as to what price it can charge, Charter resells Verizon’s mobile service at a discount. At the moment, Charter has increased its spending on mobile sales and marketing and is offering very competitive bundled packages with its broadband service to quickly build its subscription base. The company believes that the mobile service will help drive higher core product sales while improving cash flows and lowering churn over the long run. At the moment, mobile is a loss leader.

Current Outlook

- Home Depot Relative Valuation

- Walmart Relative Valuation

- CVS Relative Valuation

- Goldman Sachs Relative Valuation

- Morgan Stanley Relative Valuation

- Caterpillar Relative Valuation

- Deere Relative Valuation

- Hilton Relative Valuation

- Yum Brands Relative Valuation

- Fedex Relative Valuation

- IONS stock analysis

- Amazon Inc (AMZN) stock analysis

- Amazon Inc (AMZN) DCF Model

- Netflix (NFLX) DCF Model

- Facebook (META) DCF Model

After the TWC acquisition, Charter’s share price climbed over 250% from May 2016 through August 2021. Most of the increase was driven by the Covid lockdowns as people needed broadband to learn, work, shop, entertain themselves, and connect with co-workers, friends, and family via their home internet connections. Charter’s strong subscriber growth combined with low churn and reduced sales and marketing expenses (for video, broadband, and voice) drove operating margins into the mid-20s. By the 3rd quarter of 2021 and into 2022, the market realized that in addition to the headwind outlined above, Covid had pulled Charter’s subscriber growth forward and that marketing and churn rates would need to return to their traditional levels.

The headwinds facing Charter and the rest of the cable industry will continue to impact future growth, but they are not as disruptive as the market would have you believe. The increasing popularity of “cord cutting” has been on the rise over recent years and the trend is expected to continue for the foreseeable future. With lower revenues and higher expenses to provide pay TV, increased video churn is helping reduce a low-margin product and replace it with higher-margin broadband with increased data consumption. Over-the-top video services like Netflix and Prime Video account for roughly 70% of home broadband data consumption. When a Charter video subscriber cancels their video service, the majority remain a broadband subscriber and their data consumption increases by approximately 22%, in addition to the long-term trend of roughly 10% yearly growth.

Ongoing competition from fiber optics in the densely populated portion of its footprint is the main reason why Charter is upgrading its entire HFC network’s download and upload speeds. The entire project is expected to cost $5.5 billion and is scheduled to be completed by the end of 2025, which is significantly cheaper than running “final mile” fiber. When finished, Charter’s network will have a base download-to-upload speed of 2x1GB (using the current DOCSIS 3.1 modem), 5x1GB (Upgrading to DOCSIS 4.0 modem in 2024), and up to 10x1GB (DOCSIS 4.0 Modem) when increasing amplification on the node’s signal to 1.8 GHz. By 2025, the majority of passing will have a 5x1 capacity with the ability to upsell to 10x1. Once you get above the 2x1GB speeds, most subscribers are less concerned with speed and more focused on price.

In Charter’s rural segments, FWA is starting to gain traction. The gains are more a reflection of subscribers choosing FWA over DSL and, so far, have not had a meaningful impact on Charter’s rural subscriber base. FWA is a low-value opportunity, and deployment only makes sense in less dense areas where network capacity is underutilized. In the short run, FWA allows wireless carriers to improve their network utilization. However, in the long run, as more subscribers are added, the network’s capacity and speeds will be negatively impacted. The average broadband home consumes about 550GB of data per month. In comparison, the average mobile user consumes only 12GB of data as their phones will primarily be connected to WiFi networks throughout the day, especially when at home. Verizon charges on average $48/month for unlimited, talk, text, and data mobile subscriptions and $50/monthly for FWA plans which works out to be $4.17/GB/month vs. $0.09/GB/month respectively. One can easily see that when a wireless carrier adds a FWA subscription, it is equivalent to adding over 41 mobile subscribers to the network but at a significantly lower profit margin.

Recently, Charter has started a new growth initiative to expand its infrastructure into the rural segments of its footprint. Based on its research, portions of Charter’s rural footprint are expanding and are on the verge of developing into suburban communities that will benefit from Charter’s increased home passings. Part of this growth initiative is being buoyed by the government’s Rural Development Opportunity Fund (RDOF) which provides federal, state, and municipal grants to bring fixed broadband to millions of unserved and underserved rural households and businesses. Over the next few years, Charter plans to invest over $6 billion dollars to expand its footprint with $1.7 billion being offset by the RDOF. There is another $42 billion that will be available in the near future through the BEAD (Broadband Equity, Access, & Development) program which provides grants directly to states looking to construct/upgrade their broadband networks, subsidize low-income access, and provide development and training. These two government programs will help Charter continue to expand its rural networks.

- Apple Stock Forecast

- Netflix Stock Forecast

- Microsoft Stock Forecast

- Meta Stock Forecast

- Tesla Stock Forecast

- Amazon Stock Forecast

- Citibank Stock Forecast

- Nvidia Stock Forecast

- AMD Stock Forecast

- Best Buy Stock Forecast

- Alphabet Stock Forecast

- Home Depot Stock Forecast

- JPMorgan Stock Forecast

At the moment, Charter’s mobile segment is not profitable. Charter has purposely expanded its sales and marketing efforts in order to quickly build its mobile subscription base. The company feels that bundling mobile, especially with the internet, will attract more in-house subscribers, lower churn, and improve cash flows in the long run. There is another reason why Charter wants mobile to hit “critical mass” quickly. In 2020, Charter purchased a portion of the CBRS spectrum that corresponded with its overall footprint. When combined with its network of 25 million out-of-home WiFi access points, mostly from partnerships, Charter will be able to create its own hybrid 5G network that it can use to offload its wireless mobile subscribers and reduce the amount of data it uses from Verizon. This will amount to material savings for Charter and the network that they control.

Valuation

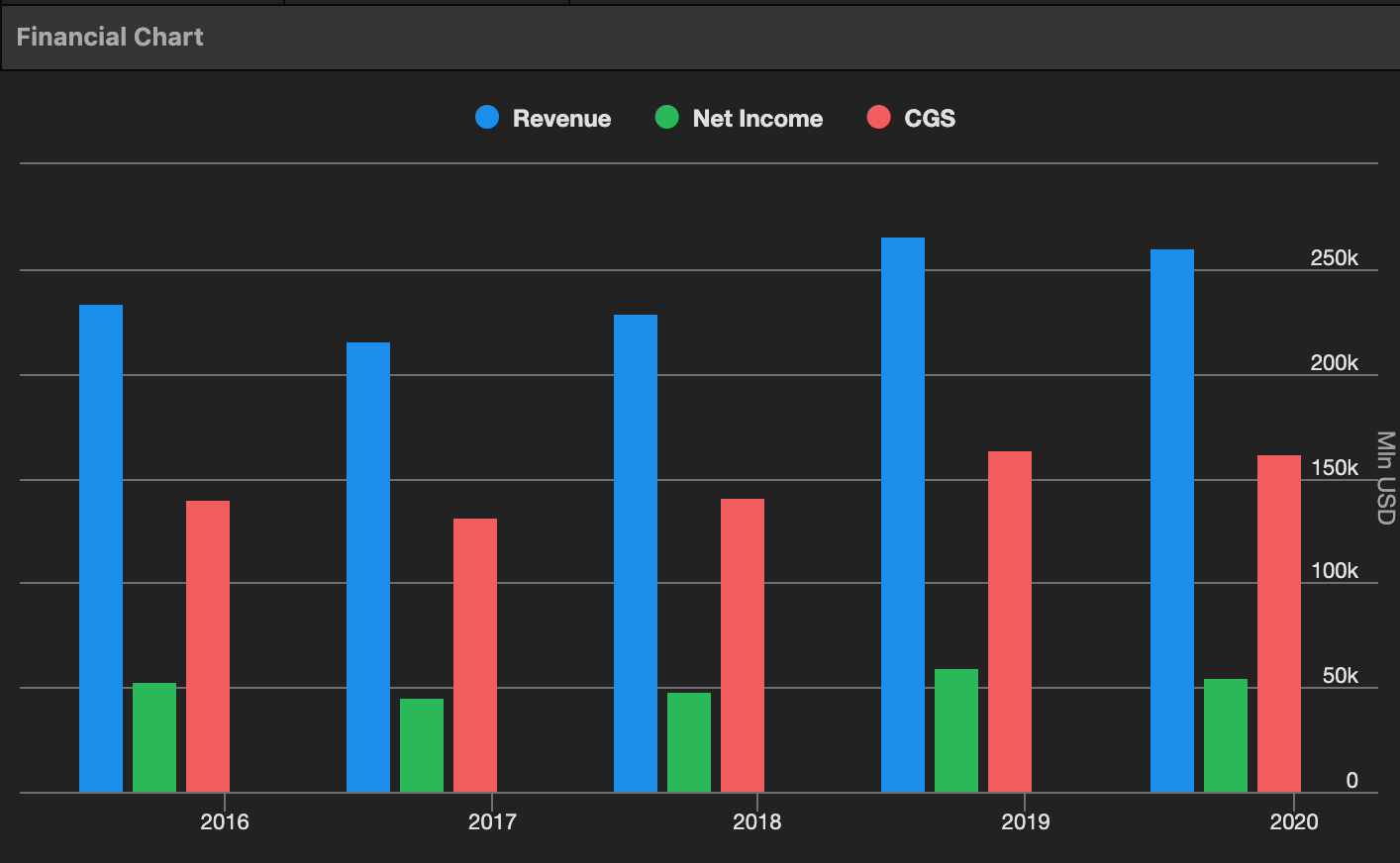

Over the next few years, Charter’s network upgrade and rural expansion will mask the company’s growing profitability. Expanded passings, an improving subscriber base, a reduction in low-margin pay TV subscriptions, and an increase in broadband subscribers and data usage will all help drive both revenue and profitability higher. Currently, shares of Charter are trading at around 12x earnings and less than 10x next year’s projected earnings. Applying a conservative 15x multiple, Charter shares would be worth around $575. For shares to rise above that level, management will need to demonstrate that they can make the mobile segment profitable, continue to buy back shares, and raise prices across the network without a mass exodus. If management can accomplish that, then shares can easily trade over $840/share.

Risks

There are a number of risks associated with an investment in Charter Communications. The most obvious is that there is no customer loyalty. Broadband, video, and mobile are all commodities, and today, it is easier than ever to switch providers. Charter has been extremely promotional in order to build up its mobile subscription base. There are no guarantees that once the promotions roll off subscribers will stay. Additionally, there are relatively very few providers of broadband which makes the government very uncomfortable adding the risk of increased government regulations. Since the acquisition of TWC and Bright House Networks, Charter has carried a high level of debt. It has not been an issue in the past because the company generates high levels of free cash flow, but it greatly limits Charter’s financial flexibility, future share repurchases, and capital expenditures, which could create an issue in the future around liquidity. Finally, it is also unclear how subscribers would react if the US economy had a downturn or an extended period of low growth.

Conclusion

Charter Communications has been under a multi-level attack over the past few years. The rise of streaming services, the expansion of fiber optics and FWA, and the growth of the mobile market have all been chipping away at the company’s business model. Charter has responded by reinvesting in its network to provide comparable upload and download speeds, expand its rural footprint, and provide its own mobile services. None of these actions will result in immediate improvements to the company’s bottom line, but over time, they will lead to increased revenues, a higher subscriber base, and improved profitability. The one card that Charter has yet to play is increasing its prices. The company has purposely kept its prices low in order to increase subscriber growth, especially in its mobile and broadband segments. This has forced the company to be hyper-vigilant about lowering expenses. If Charter can raise prices, keep its expenses in check, and not see any significant defections, the company stands to meaningfully improve its profitability. It will probably take until 2024, at the earliest, to see the network price fully implemented.

Catalyst

- Continued passings and subscriber growth.

- Reduction in low-margin pay TV subscriptions.

- Increase in broadband subscriptions & data usage.

- Mobile transition from customer acquisition cost center to profit center.

- Continue to repurchase undervalued shares.

- Raise prices across the network without a mass exodus.

For more great research, check out the recommended list of stock research platforms here.